Introduction: Can You Really Buy a Home on $23/Hour? Yes you can with this wealth plan.

If you’re 20, working hard at your first job in Canada, and earning $23/hour, the dream of buying a home feels out of reach.

After rent, car expenses, groceries, and bills, you’re left with almost nothing. Saving for a $500,000 house down payment seems impossible.

But here’s the truth: with the right money system, you can turn things around. In this post, we’ll create a 5-year wealth plan that covers:

-

Building an emergency fund 💡

-

Cutting unnecessary expenses ✂️

-

Using Canada’s most powerful investment accounts (FHSA, TFSA, RRSP) 🏦

-

Investing in ETFs for long-term growth 📈

-

Saving enough for a down payment + rainy-day fund 🌧️

By the end, you’ll see how someone on $23/hr can own a home by 25.

Step 1: Understanding the Financial Starting Point

Income

-

$23/hr × 40 hrs/week × 52 weeks = $47,840/year

-

After ~25% taxes = $35,880/year (~$2,990/month)

Expenses

-

Rent: $900

-

Car payment: $200

-

Car insurance: $200

-

Groceries + entertainment: $1,200

-

Utilities/phone/internet: $300

Total = $2,800/month

Leftover savings: only $190/month (~$2,280/year).

At this rate, you’d save just $11,000 in 5 years—not even close to a down payment. Time to optimize.

Step 2: Cutting Costs Without Killing Joy

The goal isn’t to live like a monk—it’s to spend smarter.

Car Costs

-

Current = $400/month (payment + insurance).

-

Switch: sell financed car, buy a reliable used car (~$5,000). Insurance drops to ~$150.

Savings: $250/month.

Groceries & Entertainment

-

Current = $1,200/month.

-

Plan meals, shop sales, reduce takeouts, limit subscriptions.

Savings: $300/month.

Utilities & Phone

-

Current = $300/month.

-

Switch to budget phone ($25–30/month), cut extras, reduce energy use.

Savings: $100/month.

New total savings = $840/month (~$10,080/year).

That’s a game-changer.

Step 3: Build a Rainy-Day Fund

Before investing, create a cushion.

-

Target = $10,000 emergency fund (~4–5 months of expenses).

-

At $840/month savings, it takes about 12 months.

Now you’re financially safe.

Step 4: Start Investing With ETFs

Once the emergency fund is built → it’s time to grow your money.

Why ETFs?

-

Diversification → Own 100s of companies in one fund.

-

Low fees → More of your money stays invested.

-

Strong returns → Historically, broad ETFs return 6–8% yearly.

Suggested Core Portfolio

-

VEQT (Vanguard All-Equity ETF) → High growth, global exposure.

-

XAW (iShares All-World ex-Canada) → Diversify outside Canada.

-

VGRO (Vanguard Growth ETF) → Slightly safer with 20% bonds.

Allocation: 70% VEQT + 20% XAW + 10% VGRO.

Set up automatic monthly contributions—this builds wealth while you sleep.

Step 5: Use Canada’s Wealth-Building Accounts

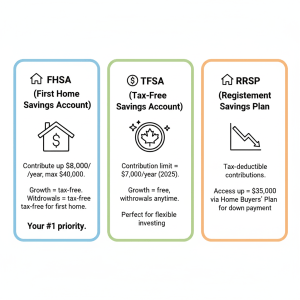

🏠 FHSA (First Home Savings Account)

-

Contribute up to $8,000/year, max $40,000.

-

Growth = tax-free. Withdrawals = tax-free for first home.

-

Your #1 priority.

🪙 TFSA (Tax-Free Savings Account)

-

Contribution limit = $7,000/year (2025).

-

Growth = tax-free, withdrawals anytime.

-

Perfect for flexible investing.

📉 RRSP (Registered Retirement Savings Plan)

-

Tax-deductible contributions.

-

Access up to $35,000 via Home Buyers’ Plan for down payment.

Strategy:

-

Max FHSA ($8k/year).

-

Use TFSA for extra ($2k–3k/year).

-

Use RRSP once FHSA + TFSA filled.

Step 6: 5-Year Wealth Plan

Year 1

-

Build $10,000 emergency fund.

-

Learn budgeting & investing basics.

Year 2

-

Open FHSA + TFSA.

-

Contribute $8k FHSA + $2k TFSA.

-

Start ETF investing.

Year 3

-

FHSA $8k + TFSA $2k + RRSP $2k.

-

Total invested = ~$20,000.

Year 4

-

FHSA $8k + TFSA $2k + RRSP $3k.

-

Investments = ~$40,000 (with growth).

Year 5

-

Max FHSA ($40k). Add TFSA $2k + RRSP $5k.

-

Investments = $65,000–70,000 (with growth).

Step 7: Can You Afford the House?

Target = $500,000 house.

-

Minimum down payment = $25,000 (5%).

-

Closing costs + fees = ~$10,000.

-

Keep emergency fund = $10,000.

Needed = ~$45,000.

You’ll have $65k+ saved in 5 years, covering all costs plus a buffer.

Inflation & Income Growth

-

Inflation = ~3%/year (groceries, rent rise).

-

Wage growth = ~3%/year.

-

By Year 5 → wage = ~$26/hr (~$3,300/month net).

This keeps the plan realistic.

Final Picture at Age 25

-

Emergency fund = $10,000

-

Investments = $65,000–70,000

-

Home down payment ready = $45,000

-

Extra wealth = $20,000+ growing

Why This Works

-

Focuses on cash flow first.

-

Builds a safety net before investing.

-

Uses Canada’s tax-advantaged accounts.

-

Keeps investing simple with ETFs.

-

Provides a step-by-step 5-year roadmap.

⚠️ Disclaimer

This blog presents a hypothetical financial scenario intended purely for educational purposes. Every individual’s financial situation is unique, and factors such as income, expenses, risk tolerance, and goals will differ. The strategies and investment examples provided here (including TFSA, RRSP, FHSA, and ETFs) should not be taken as personalized financial advice.

Before making any financial decisions, it is strongly recommended that you consult with a certified financial planner or advisor who can tailor a plan to your specific needs.

For more details, please visit the full Disclaimer Page here.

Further Reading:

| Title | Author(s) | Why It’s Valuable |

|---|---|---|

| Money 101: Every Canadian’s Guide to Personal Finance | Ellen Roseman | A simple crash course for beginners, covering budgeting, saving, and credit basics from a Canadian perspective. |

| Beat the Bank: The Canadian Guide to Simply Successful Investing | Larry Bates | Explains how to invest smartly in Canada, avoid high fees, and build wealth with ETFs and index funds. |

| Personal Finance for Canadians | Elliot Currie et al. | Covers savings, debt management, and investing with a clear structure tailored to Canadian tax rules. |

| Personal Finance For Canadians For Dummies | Eric Tyson & others | Beginner-friendly with step-by-step guidance on RRSPs, TFSAs, budgeting, and more. |

| A Canadian’s Guide to Money-Smart Living | Kelley Keehn & Alex Fisher. | Focuses on building smarter money habits and everyday financial decision-making for Canadians |