Introduction — Why ETFs are like vending machines for investments (and exactly why that’s awesome)

Imagine a vending machine that gives you a tiny piece of dozens, hundreds, or even thousands of companies for the price of one snack. Instead of buying one candy bar (one stock), you buy a whole snack pack (an ETF) that has fruit, cereal, crackers — everything. No wrestling with which single snack will taste best. You get variety instantly.

That’s what an ETF does for your money. A single ETF share is a small slice of a basket of stocks, bonds, or other assets. For Canadian investors the TSX (Toronto Stock Exchange) lists many ETFs that are easy to buy, usually low-cost, and ideal for building a long-term plan.

This chapter is your step-by-step, plain-English guide to:

-

What ETFs are and how they work.

-

The different types of TSX ETFs and when to use each.

-

How to choose ETFs (fees, liquidity, tracking error).

-

Where to hold ETFs (TFSA vs RRSP vs non-registered) and tax tips.

-

Covered calls, dividend strategies, bond ETFs and how to combine them into model portfolios.

-

Practical next steps to start or refine your own portfolio.

Let’s begin.

What is an ETF? (Explained like you’re 12)

An ETF (Exchange-Traded Fund) is a special kind of financial product that packages many investments into one share. Think of it like a school lunchbox filled with a variety of snacks — when you buy the lunchbox, you get a bit of everything inside.

Key points:

-

You can buy and sell ETFs any time the stock market is open — like buying a movie ticket while the cinema is open.

-

ETFs can hold stocks, bonds, commodities, or a mix.

-

ETFs usually have low fees called MERs (Management Expense Ratio). If the MER is 0.05%, that’s $5 a year on $10,000 invested.

-

They give instant diversification — so one bad company generally won’t ruin your whole lunchbox.

Why ETFs beat picking single stocks for most people:

Buying many good companies automatically reduces risk. Unless you’re a professional research wizard, it’s hard to pick winners. ETFs provide a simple, low-cost way to own the market.

The Main Types of TSX ETFs and How to Use Them

Below are the categories you’ll find on the TSX. For each I give a super simple description, who it’s good for, typical risks, and examples (tickers included).

1) Broad Market Equity ETFs — Your portfolio’s engine

What: These ETFs own a large chunk of a given market (all Canada, the U.S., global).

Why use them: Core building block for long-term growth.

Risk: They’re still stocks, so prices can swing up and down.

Examples: XIC (iShares Core S&P/TSX Capped), VCN (Vanguard FTSE Canada All Cap), VFV (Vanguard S&P 500 ETF – provides US exposure in Canadian dollars), XAW (iShares Core MSCI All Country World ex Canada).

How to think about them (12-year-old version):

If the world’s companies are a big cake, a broad ETF gives you a fair slice of that cake. Over time that slice usually grows.

2) Dividend ETFs — Income without doing the math

What: ETFs that focus on companies that pay dividends (cash payouts).

Why use them: Good for regular income (e.g., retirees or income-focused savers).

Risk: Can be concentrated in certain industries (like banks, energy). Dividends can be cut in bad times.

Examples: VDY (Vanguard FTSE Canadian High Dividend Yield), CDZ (iShares Canadian Dividend Aristocrats), ZWC (BMO Canadian High Dividend Covered Call — explained next).

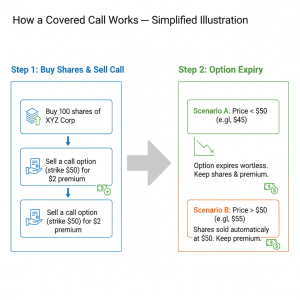

Covered Calls (explained simply and in depth):

A covered call is a strategy that earns income from shares you already own. It’s like renting out a ticket you own to someone else for a fee. You get paid the fee now. If the price of the ticket goes way up, the renter gets to buy it at a price you agreed on — you missed some extra profit but you kept the fee.

Example with numbers (easy):

-

You own 100 shares of a stock at $50.

-

You sell a call option with strike price $55 for $2 per share. You collect $200 (100 x $2) now.

-

If the stock stays below $55, you keep the $200 and still own the stock.

-

If the stock goes above $55, your stock may be called away (sold at $55). You still keep the $200, but you miss the extra upside above $55.

Covered call ETFs (like ZWC) sell these options across a basket of stocks automatically to create higher distributions (monthly cash). They are popular for income, but they cap upside during strong bull markets.

3) Sector & Thematic ETFs — The spice cabinet of investing

What: Focus on one industry (tech, energy) or theme (AI, cybersecurity).

Why use them: If you believe a sector will grow faster than the market, these let you overweight it.

Risk: Very high — fewer companies means bigger swings.

Use as: Small “satellite” positions inside a bigger, diversified portfolio.

Examples: XIT (Canadian tech ETF), CYBR (cybersecurity), HGU (leveraged gold miners — high risk).

4) Fixed Income (Bond) ETFs — The shock absorbers

What: Hold government or corporate bonds.

Why use them: Reduce volatility, provide income, protect capital.

Risk: Interest rates go up → bond prices drop. Credit risk if a company defaults.

Examples: VAB (Vanguard Canadian Aggregate Bond ETF), XBU (iShares Core Canadian Universe Bond ETF), XSB (iShares short-term bond ETF).

Why bond ETFs?

If the stock market is a rollercoaster, bonds are the brakes. They won’t give huge long-term growth, but they help you sleep better at night.

5) ESG ETFs — Invest with values

What: ETFs that exclude or favor companies with strong Environmental, Social, Governance practices.

Why use them: Align investing with your values.

Note: “ESG” means different things across funds — read the fund’s rules and holdings.

Examples: ESGA (BMO MSCI Canada ESG Leaders), XUSR (iShares ESG Aware MSCI USA).

ETF Mechanics: Fees, Liquidity, Tracking Error & Structure

MER: management expense ratio

-

MER is the ongoing fee the fund charges every year.

-

Example: MER 0.05% on a $10,000 investment costs about $5 / year. MERs matter: small differences compound over decades.

Trading costs: commissions and bid-ask spreads

-

When you buy an ETF you may pay a commission (some brokers are free) and a tiny markup between buy & sell price (the spread). Choose ETFs with good liquidity (higher AUM & volume) to keep spreads tight.

Tracking error

-

The difference between an ETF’s performance and the index it’s supposed to match. Small is fine; big is a problem.

ETF structure: physically-backed vs synthetic

-

Physical ETF owns the underlying stocks/bonds.

-

Synthetic ETF uses derivatives to replicate returns. Synthetic may be cost-efficient but adds counterparty risk. For most retail investors, physical is easier to understand and safer.

Where to Hold ETFs in Canada (TFSA, RRSP, RESP, Non-Registered)

This choice affects taxes and ultimately how much money stays in your pocket. Short, plain rules follow — with authoritative sources cited.

Quick plain summary:

-

TFSA (Tax-Free Savings Account): Investment growth and withdrawals are tax-free in Canada. BUT dividends from U.S. stocks or U.S.-listed ETFs can be subject to U.S. withholding tax (typically reduced to 15% under the Canada-U.S. tax treaty) and that withheld tax is not recoverable in a TFSA. So be careful with US dividend ETFs in TFSA. BlackRock+1

-

RRSP (Registered Retirement Savings Plan): Tax-deferred. U.S. dividends held inside an RRSP are generally exempt from the U.S. withholding tax due to the Canada-U.S. tax treaty (so U.S dividend ETFs often belong in RRSPs rather than TFSAs). Talk to your broker/tax advisor and ensure necessary forms are completed. IRS+1

-

Non-Registered Account: Dividends from U.S. stocks are usually subject to the 15% withholding, but you may be able to claim foreign tax credits on your Canadian tax return. BlackRock+1

Forms & practical TIP: Complete the W-8BEN form (or relevant documentation) to claim treaty rates and avoid higher default withholding rates. Your brokerage often takes care of this but check. Canada.ca

What this means in practice:

-

If you plan to hold U.S. dividend-paying funds, an RRSP is often the most tax-efficient shelter.

-

If you want tax-free growth and withdrawals (for Canadian gains/capital gains), TFSA is great — but avoid U.S. dividend-heavy ETFs in TFSA because of the unrecoverable withholding.

-

For Canadian dividend ETFs, TFSA is excellent because Canadian dividends are not subject to the same U.S. withholding rules.

Quick example (simple math): If an ETF pays $100 in U.S. dividends and 15% is withheld, you only receive $85. Over time, unrecoverable withholding reduces your compounding.

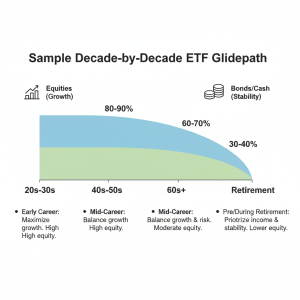

Model Portfolios: “By Age” — Practical, step-by-step

These are templates — adapt to your comfort with risk and personal goals.

20s — Aggressive Accumulator (90% stocks / 10% bonds)

-

Why: Long time horizon = take more risk for more growth.

-

Sample ETFs: 30% VCN (Canada), 40% VFV/XAW (U.S & global), 20% XEQT (global all-equity), 10% VAB (bonds)

-

Notes: Use TFSA + RRSP to shelter growth. Focus on low fees & automatic monthly investing.

30s — Strategic Builder (80% / 20%)

-

25% XIC (Canada), 35% XAW (global), 20% VGRO (all-in-one), 20% XBU (bonds)

-

Add small satellite positions (e.g., 5% tech/theme) if you want.

40s — Peak Accumulator (60% / 40%)

-

20% Canadian Equity, 25% Global Equity (XAW), 15% Dividend ETFs (VDY), 40% Bonds (VAB/XSB mix)

-

Start shifting for shorter-term goals (e.g., house, school).

50s — Pre-Retirement Transition (50% / 50%)

-

15% Canada, 20% Global, 15% Dividend ETFs, 50% Bonds (shorter duration favored), cash reserve.

60s+ — Retirement Income Phase (30% / 70% bonds & cash)

-

10% Canada equities, 10% global equities, 10% dividend ETFs (for income), 50% bonds, 20% cash equivalents (near-term expenses).

How much to save per month?

No single right answer — but automate. If you can automate 10%–20% of income into the above allocation, you’ll compound a lot over decades. For more money saving tips read the blog post on budgeting to help you save for investing here.

Covered Calls, Income Strategies & When to Use Them

We explained covered calls earlier — here’s a longer look, simple math, and real-world use:

Covered call ETF pros:

-

Higher current income (monthly distributions).

-

Lower volatility in downturns (premiums cushion drops).

Covered call ETF cons:

-

Capped upside — you won’t capture full stock rallies.

-

Options strategies can add tracking error to the index.

Who should consider covered call ETFs?

-

Investors needing regular cash flow (retirees), or those willing to trade some upside for steadier income.

Practical tip:

If you want both growth and income, consider keeping a “core” growth ETF (like XAW or XEQT) and a small allocation (10–20%) to a covered call ETF.

How to Pick an ETF: A Simple Checklist

-

Objective & holdings: Does the ETF actually own the assets you want? (Read the fact sheet.)

-

MER: Lower is usually better — small differences matter long term.

-

AUM & Liquidity: Bigger funds and higher trading volume = tighter spreads.

-

Tracking error: Check historical tracking vs. index. Smaller is better.

-

Distribution policy: Monthly/quarterly? Cash/distribution reinvestment?

-

Structure: Physical vs synthetic. Preference: physical for simplicity.

-

Tax considerations: Which account will hold it? (see Chapter 4)

-

Sponsor & provider: Do you trust Vanguard, iShares, BMO, Horizons?

-

Use case: Core holding vs satellite (theme) vs income play.

Rebalancing, Automatic Investing & Simple Rules

-

Automatic investments: Set up monthly purchases (dollar-cost averaging). Automate transfers from your bank to brokerage.

-

Rebalance schedule: Once or twice a year is fine (rebalance when allocation drifts >5% from target).

-

Rule of thumb: Keep core holdings (broad market ETFs) as the bulk; theme/sector ETFs remain small.

Common Mistakes & How to Avoid Them (short and sweet)

-

Chasing hot sectors with large positions. → Avoid overconcentration.

-

Ignoring fees. → Small MERs compound.

-

Putting U.S. dividend ETFs into TFSA without checking withholding tax. → Refer to Chapter 4. BlackRock

-

Forgetting to rebalance. → Rebalance annually or on drift.

-

Not checking ETF holdings. → Always read the fact sheet.

Putting it All Together: A 6-Step Action Plan

-

Pick your core (broad market ETF for Canada + U.S/global).

-

Choose your account (TFSA for Canadian equity & tax-free growth; RRSP for US dividend exposure). Canada.ca+1

-

Set up automatic monthly buys.

-

Use a small amount for satellite bets (sector/theme) — no more than 5–10% each.

-

Rebalance yearly.

-

Keep learning — read fund fact sheets and watch MERs.

Further Reading & Resources

-

Reboot Your Portfolio — Dan Bortolotti (Canadian Couch Potato)

-

BMO / Vanguard / iShares — ETF provider fact sheets

-

CRA TFSA guide (for account rules). Canada.ca

Frequently Asked Questions (FAQ)

Q1: Are ETFs safer than individual stocks?

A1: ETFs are usually less risky than owning a single stock because they spread your money across many companies. But the market itself can fall, so they are not risk-free.

Q2: Should I use TFSA or RRSP for my ETFs?

A2: Use TFSA for Canadian equity & growth ETFs. Use RRSP for US dividend ETFs (to avoid U.S. withholding tax). For details and broker setup, consult a tax advisor. BlackRock+1

Q3: What is a covered call ETF and who should own it?

A3: It’s an ETF that sells call options on stocks it owns to generate extra income. Good for income-seeking investors, but it caps upside in big rallies.

Q4: How much should I put into bonds as I get older?

A4: A simple rule is to increase bond allocation as you age (e.g., 60s → more bonds). See the decade templates above for specifics.

Q5: Do ETFs pay dividends?

A5: Some ETFs distribute dividends if the underlying holdings pay dividends. Others accumulate. Always check the ETF’s distribution policy.

Important Disclaimer

Important Disclaimer

The information contained in this blog post is provided for general educational and self-study purposes only. It is intended to deepen your understanding of Exchange-Traded Funds (ETFs) available on the TSX and is not a substitute for professional, personalized financial advice.

No Financial Advice: This content does not constitute investment, financial, legal, or tax advice. The model portfolios, fund examples, and strategies discussed are for illustrative and educational purposes only and may not be suitable for your individual financial situation, risk tolerance, or investment objectives.

No Endorsement or Guarantee: Mention of any specific ETF or provider is for informational purposes and should not be interpreted as an endorsement or recommendation. Past performance is not indicative of future results, and all investments carry risk, including the potential loss of principal. For this reason, specific return figures have been deliberately omitted to avoid any misinterpretation that this blog should be the basis for your financial planning.

Essential Steps Before Investing:

-

Seek Professional Guidance: We strongly advise you to consult with a qualified, certified financial planner (CFP) or other accredited financial advisor before making any investment decisions. They can provide advice tailored to your unique circumstances.

-

Conduct Your Own Research: You must carry out your own independent due diligence. This includes reviewing the ETF’s official prospectus, fact sheet, and other regulatory documents to understand its objectives, strategies, fees, and risks fully.

In summary, this blog is a starting point for your education, not a finishing line for your investment decisions. The responsibility for any investment choices you make rests solely with you.