The Ultimate Guide to Reducing Insurance Costs in Canada: Smart Strategies for Auto, Home, Life, Disability, and Accident Insurance

Insurance is a non-negotiable part of responsible financial planning in Canada, but that doesn’t mean you should overpay for coverage. With insurance premiums rising across the board—particularly for auto and home insurance—understanding how to optimize your coverage while minimizing costs has never been more important.

This comprehensive guide will walk you through proven strategies to reduce your insurance costs across all major categories, and provide age-specific and gender-based recommendations to help you build the ideal insurance portfolio throughout your life.

Understanding the Current Insurance Landscape in Canada (2025)

Before diving into cost-reduction strategies, it’s important to understand why insurance costs have been rising. In 2025, Ontario homeowners are paying an average of 5.45% more for home insurance compared to last year. Meanwhile, auto insurance claims in Ontario reached a staggering 190% claims ratio in 2023, meaning insurers paid out $1.90 for every dollar collected in premiums—driving significant rate increases.

The good news? Despite these increases, there are numerous strategies you can employ to bring your costs down significantly.

AUTO INSURANCE: STRATEGIES TO DRIVE DOWN YOUR RATES

Auto insurance is mandatory across Canada, and for many households, it’s one of the largest insurance expenses. With the average cost of car ownership exceeding $16,000 annually (including insurance, gas, and maintenance), every dollar saved on premiums matters.

1. Maintain a Clean Driving Record

Your driving record is the single most influential factor in determining your auto insurance rates. Insurers reward safe drivers because they represent lower risk. Here’s how to leverage this:

- Accident-Free Discounts: Many insurers offer discounts to drivers who haven’t had accidents for a certain period (typically 3-6 years)

- Violation-Free Status: Even minor traffic tickets can increase your premium by 10% or more. A first minor conviction (like speeding) typically adds 10% to your rate

- Defensive Driving Courses: Some insurers offer discounts if you complete an approved defensive driving course

Pro Tip: If your driving habits have changed—perhaps you’re working from home or using public transit more—inform your insurer immediately. Reduced annual mileage can lead to premium reductions.

2. Leverage Usage-Based Insurance (Telematics)

Usage-based insurance programs track your actual driving habits through a mobile app or device installed in your car. These programs can offer savings of 15-35% for safe drivers who:

- Avoid harsh braking and rapid acceleration

- Drive during lower-risk hours (avoiding late-night driving)

- Maintain consistent, moderate speeds

- Log fewer miles overall

Programs like these are particularly beneficial for urban drivers who have access to public transportation and don’t drive daily.

3. Adjust Your Deductibles Strategically

A deductible is the amount you pay out-of-pocket before your insurance kicks in. By agreeing to a higher deductible, you can significantly lower your annual premium:

- Increasing from a $500 to $1,000 deductible can reduce yearly premiums by 15-25%

- Consider your financial cushion: only choose a higher deductible if you can afford to pay it in an emergency

- For older vehicles, evaluate whether comprehensive and collision coverage are worth maintaining

Important Balance: Never reduce liability coverage to save money. Liability protects you if you cause an accident resulting in damage or injury to others, and inadequate coverage can leave you financially devastated.

4. Bundle Your Policies

Combining your auto insurance with home insurance (or other policies) under one provider can unlock substantial savings—often 15-20% off your total premiums. This “multi-policy discount” is one of the easiest ways to save.

5. Install Anti-Theft Devices

Vehicle theft claims in Canada surpassed $1.5 billion in 2023, with Ontario hit particularly hard. Installing anti-theft equipment can:

- Save $500-$1,000 annually on premiums

- Prevent surcharges of $500-$1,500 from some insurers for high-risk vehicles

- Qualify you for safe-parking discounts if your vehicle is stored in a private garage

Consider GPS tracking devices, steering wheel locks, or alarm systems monitored 24/7.

6. Take Advantage of Winter Tire Discounts

Many Canadian insurers offer discounts (typically 2-5%) for drivers who install winter tires. Not only do winter tires improve safety in harsh conditions, but they also demonstrate to insurers that you’re reducing your accident risk.

7. Choose Your Vehicle Wisely

Your vehicle’s make, model, and year significantly impact insurance costs:

- Lower Insurance Vehicles: Chrysler, Chevrolet, GMC, Buick models typically have lower premiums

- Higher Insurance Vehicles: Sports cars, luxury vehicles, and commonly stolen models (like the 2021 Toyota Highlander) carry higher premiums

- Consider Repair Costs: Vehicles with expensive parts or sophisticated technology cost more to insure

Check insurance costs before purchasing a vehicle, not after.

8. Improve Your Credit Score

In provinces where it’s permitted (Alberta, New Brunswick, PEI, Quebec, and Nova Scotia), insurers can use credit scores to determine premiums. A better credit score can lead to more favorable rates. Focus on:

- Paying down high-interest debt (especially credit cards)

- Making consistent, on-time payments

- Avoiding opening new credit lines unnecessarily

9. Ask About Specialized Discounts

Many insurers offer discounts you may not know about:

- Alumni Discounts: Membership in certain alumni groups or professional associations

- CAA Membership: CAA members often receive special insurance discounts

- Low-Mileage Discounts: If you drive under a certain threshold annually

- Group Rates: Employees of large companies may qualify for group rates

10. Shop Around Annually

Canada’s insurance market is competitive. Comparing rates from multiple insurers can reveal significant savings—sometimes $1,000+ annually for the same coverage. Use online comparison tools or work with an independent insurance broker who can shop multiple companies on your behalf.

Critical Note: Wait until your renewal date to switch insurers to avoid mid-term cancellation penalties.

HOME INSURANCE: PROTECTING YOUR BIGGEST INVESTMENT AFFORDABLY

Home insurance isn’t legally required in Canada, but if you have a mortgage, your lender will require it. With the average Ontario home insurance cost around $1,423 annually (and $1,814 in Toronto), finding savings is crucial.

1. Bundle with Auto Insurance

Just as with auto insurance, bundling your home and auto policies with the same provider can save you 15-20% on total premiums. This is one of the most straightforward savings strategies.

2. Increase Your Deductible

Similar to auto insurance, choosing a higher deductible significantly reduces your yearly premiums. Common deductibles range from $500 to $2,500:

- Moving from $500 to $1,000 deductible: ~15% savings

- Moving from $1,000 to $2,500 deductible: ~25-30% savings

Ensure you have emergency savings to cover the deductible if needed.

3. Invest in Home Improvements That Reduce Risk

Certain home upgrades can lower your premiums by demonstrating reduced risk:

Roof Replacement:

- A new roof (especially if your current roof is 20+ years old) can decrease premiums by 5-15%

- Metal or recycled rubber roofs may qualify for additional discounts

- Some insurers may require roof replacement for older homes

Plumbing and Electrical Updates:

- Replacing old galvanized or lead pipes reduces water damage risk

- Updating knob-and-tube wiring or bringing electrical systems up to code

- Some insurers require these updates for older homes (50+ years)

- Replacing hot water tanks older than 10 years

Water Damage Prevention:

- Installing sump pumps can reduce premiums by 5-10%

- Water shut-off systems and water sensor alarms

- Sewer backwater valves to prevent basement flooding

Security Systems:

- Centrally monitored alarm systems can save up to 10% on premiums

- Video doorbells and security cameras

- Fire alarms and automatic sprinkler systems

- Monitored systems provide greater discounts than unmonitored ones

4. Avoid Over-Insuring Your Home

When calculating replacement cost, don’t include the value of the land—only the cost to rebuild the structure with like-quality materials. Over-insuring wastes money on unnecessary coverage.

Review your coverage annually to ensure it matches your actual replacement needs, not the inflated market value of your property.

5. Add Sewer Backup and Overland Flood Coverage

While this seems counterintuitive to saving money, these coverages can prevent catastrophic out-of-pocket expenses. With extreme weather events causing $8.5 billion in insured damages in Canada in 2024, targeted coverage for your highest risks is essential.

Sewer backup coverage costs $100-300 annually but can save tens of thousands in basement flooding damage.

6. Maintain Your Home Regularly

Regular maintenance prevents larger claims down the line:

- Clean gutters and downspouts

- Inspect and maintain your roof

- Address plumbing leaks immediately

- Keep trees trimmed away from your house

- Winterize pipes in colder months

The fewer claims you file, the lower your premiums remain.

7. Consider Paying Annually

Some insurers offer 5-8% discounts if you pay your entire annual premium upfront rather than in monthly installments. If your cash flow allows, this simple change adds up over time.

8. Consent to a Soft Credit Check

A soft credit check (which doesn’t affect your credit score) allows insurers to determine your best price and level of discount. Better credit typically equals better rates.

9. Quit Smoking

Yes, smoking status affects home insurance rates. Smokers pay higher premiums due to increased fire risk. Quitting smoking benefits your health and your wallet.

10. Shop the Market

Don’t automatically renew with your current insurer. Compare quotes from multiple providers every 1-2 years. Insurance brokers can help you compare options from multiple companies quickly and efficiently.

LIFE INSURANCE: SECURING YOUR FAMILY’S FUTURE WITHOUT BREAKING THE BANK

Life insurance is essential for anyone with dependents, debt, or financial obligations that would burden loved ones after their death. The good news? Life insurance is often more affordable than people expect—especially if purchased young.

1. Buy Life Insurance While You’re Young and Healthy

This is the single most important strategy for affordable life insurance. Premiums are locked in at the rate you qualify for when you purchase:

- A 30-year-old may pay $20-40/month for $500,000 coverage

- A 50-year-old may pay $100-200/month for the same coverage

- Premiums can double or triple between age 30 and age 50

Every year you wait, premiums increase. Lock in low rates early.

2. Choose Term Life Insurance Over Permanent (For Most People)

For the vast majority of Canadians, term life insurance provides all the coverage needed at a fraction of the cost of permanent insurance:

- Term Life: Coverage for a specific period (10, 20, or 30 years); premiums are much lower

- Permanent Life: Lifetime coverage with cash value component; significantly more expensive

Unless you have specific estate planning needs, permanent life insurance is often unnecessary and expensive.

3. Calculate Exactly How Much Coverage You Need

Don’t over-insure. Calculate your coverage needs based on:

- Outstanding mortgage balance

- Other debts (car loans, credit cards, student loans)

- Income replacement (typically 5-10 years of salary)

- Children’s education costs

- Final expenses (funeral, estate settlement)

Many people buy more insurance than necessary, wasting premium dollars.

4. Maintain a Healthy Lifestyle

Life insurance premiums are heavily influenced by health factors:

- Quit smoking: Smokers pay 2-3x more than non-smokers

- Maintain healthy weight: Obesity significantly increases premiums

- Manage chronic conditions: High blood pressure, diabetes, and heart conditions increase costs

- Avoid risky hobbies: Rock climbing, skydiving, and similar activities may increase rates

5. Bundle with Disability Coverage

Some insurers offer discounts when you bundle life insurance with disability insurance. This provides comprehensive protection at a reduced rate.

6. Maximize Employer Benefits First

If your employer offers group life insurance, take full advantage—it’s typically less expensive than individual policies and may not require medical exams up to a certain coverage amount. However:

- Don’t rely solely on employer coverage (it disappears if you change jobs)

- Use employer coverage as a supplement to your own individual policy

7. Shop Multiple Insurers

Life insurance rates vary significantly between companies. Comparing quotes from 5-10 insurers can reveal savings of 20-40% for identical coverage. Work with an independent broker who can access multiple carriers.

8. Consider Convertibility Options

If you purchase term life insurance, ensure it has a conversion option that allows you to convert to permanent coverage later without a medical exam. This provides flexibility as your needs change.

DISABILITY INSURANCE: PROTECTING YOUR INCOME

Disability insurance replaces your income if illness or injury prevents you from working. Given that 40% of Canadians become disabled for 90+ days before age 65, this coverage is crucial yet often overlooked.

1. Start with Employer Group Coverage

If available, maximize your employer’s group disability insurance. It’s typically:

- Less expensive than individual policies

- May require no medical exam up to certain coverage limits

- Premiums may be partially or fully paid by your employer

However, group coverage often provides only 60-70% income replacement, so consider supplementing with individual coverage.

2. Choose Longer Waiting Periods

The waiting period (elimination period) is the time between becoming disabled and when benefits begin. Longer waiting periods dramatically reduce premiums:

- 30-day waiting period: Higher premiums

- 90-day waiting period: Moderate premiums (most common)

- 180-day waiting period: Lower premiums

If you have 6-12 months of emergency savings, opt for a longer waiting period to reduce costs by 20-40%.

3. Select Appropriate Benefit Periods

Benefit periods determine how long you’ll receive payments:

- 2-year benefit period: Lowest cost

- 5-year benefit period: Moderate cost

- To age 65: Highest cost (but best protection)

Choose based on your savings cushion and risk tolerance. For most people, coverage to age 65 provides the most comprehensive protection.

4. Tailor Coverage to Your Actual Income Needs

Most disability policies replace 60-85% of your income. Calculate exactly what you’d need to cover:

- Mortgage/rent

- Food and utilities

- Transportation

- Other essential expenses

Don’t over-insure—select coverage that meets your needs without excess.

5. Apply While Young and Healthy

Just like life insurance, disability insurance premiums increase with age and health conditions. Typical costs:

- 20s-30s: 1-2% of annual income

- 40s-50s: 2-3% of annual income

Lock in lower rates early, especially if you work in a physically demanding occupation.

6. Consider “Any Occupation” vs. “Own Occupation” Carefully

- Own Occupation: Pays benefits if you can’t perform your specific job (more expensive but better protection)

- Any Occupation: Pays only if you can’t work in any job suitable to your skills (cheaper but harder to qualify for benefits)

For most people, “own occupation” provides adequate protection at reasonable cost.

7. Be Strategic with Optional Riders

Riders increase coverage but also increase costs. Essential riders include:

- Cost of Living Adjustment (COLA): Increases benefits with inflation

- Future Insurability Option: Allows purchasing more coverage later without medical exam

- Residual Benefits: Pays partial benefits if you return to work part-time

Skip riders you don’t need to keep premiums manageable.

8. Leverage Occupational Class Discounts

Some insurers offer 20% premium reductions for professionals in low-risk occupations:

- Software professionals

- Accountants

- Engineers

- Medical specialists

- Lawyers and judges

- Architects

If you work in a desk-based profession, shop for insurers offering professional class discounts.

9. Pay Premiums Yourself (Not Through Employer)

If you pay disability premiums with after-tax dollars (rather than your employer paying), your benefits will be tax-free if you ever need to claim. This effectively increases your benefit by 20-30%.

10. Shop the Market

Disability insurance rates vary dramatically between providers. Compare quotes from multiple insurers to find the best combination of coverage and cost.

ACCIDENT INSURANCE: AFFORDABLE SUPPLEMENTAL PROTECTION

Accident insurance is less common but can be valuable for specific situations. This coverage pays a lump sum or ongoing benefits if you’re injured in an accident (regardless of fault).

Cost-Saving Strategies:

- Evaluate if You Already Have Coverage: Check if your employer benefits, credit card, or travel insurance already include accident coverage before purchasing standalone policies

- Purchase Only What You Need: Accident insurance should supplement, not replace, disability and health insurance

- Compare Group Plans: Some professional associations and alumni groups offer accident insurance at group rates

- Consider Coverage Limits Carefully: Higher coverage amounts cost more; select amounts that genuinely fill gaps in your coverage

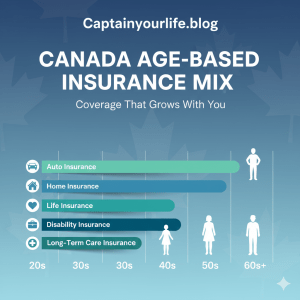

THE IDEAL INSURANCE MIX BY AGE AND LIFE STAGE

Your insurance needs change throughout life. Here’s a comprehensive guide to building the optimal insurance portfolio at each stage.

AGES 18-29: BUILDING YOUR FOUNDATION

At this stage, you’re likely starting your career, may be renting, and possibly single without dependents. Your insurance needs are relatively modest but important.

Essential Coverage:

Auto Insurance (if you own a vehicle):

- Minimum mandatory coverage in your province

- Consider higher liability limits ($1-2 million) for better protection

- Skip comprehensive/collision on very old vehicles

- Take advantage of good student discounts if applicable

- Monthly Cost: $150-300 (varies significantly by province and driving record)

Renters Insurance:

- Protects personal belongings and provides liability coverage

- Often required by landlords

- Monthly Cost: $15-30

- Bundle with auto insurance for discounts

Life Insurance:

- If you have co-signed loans, parents who depend on you, or plan to marry soon

- Term life insurance: $250,000-500,000 coverage

- 20-30 year term locks in low rates for decades

- Monthly Cost: $20-40 for $500,000 coverage

- Important: Even if you don’t need coverage yet, buying now locks in the lowest rates for life

Disability Insurance:

- Critical if you don’t have group coverage through an employer

- Your ability to earn income is your most valuable asset

- Opt for 90-day waiting period to reduce costs

- Monthly Cost: $30-60 (1-2% of income)

- Priority Level: High if self-employed or no employer coverage

What You Can Skip:

- Home insurance (unless you own property)

- Permanent life insurance

- Long-term care insurance

Total Approximate Monthly Investment: $200-400

AGES 30-39: GROWING RESPONSIBILITIES

This decade typically brings major milestones: marriage, first home purchase, starting a family, and career advancement. Your insurance needs increase significantly.

Essential Coverage:

Auto Insurance:

- Maintain comprehensive coverage if you have a newer vehicle

- Increase liability limits to $2 million as your net worth grows

- Consider umbrella liability insurance if net worth exceeds $500,000

- Monthly Cost: $150-350

Home Insurance (if you own):

- Mandatory for mortgage holders

- Ensure adequate replacement cost coverage

- Add sewer backup and overland flood coverage

- Monthly Cost: $100-200

Life Insurance:

- Critical once you have children or a mortgage

- Term life insurance: $500,000-$1,000,000 coverage per working spouse

- 20-30 year term to cover until kids are independent and mortgage is paid

- Monthly Cost: $40-80 for $750,000 coverage

- Consider: Spouse with lower income should also have coverage (often overlooked)

Disability Insurance:

- Non-negotiable at this stage—you have dependents relying on your income

- Maximize employer group coverage, supplement with individual policy if needed

- Target 60-75% income replacement

- Monthly Cost: $100-200 (1.5-2.5% of income)

- Don’t skip this: 1 in 3 people will be disabled for 90+ days before age 65

Critical Illness Insurance (Optional):

- Provides lump sum if diagnosed with major illness (cancer, heart attack, stroke)

- Useful if you lack emergency savings or have family history of illness

- Monthly Cost: $50-150 depending on coverage amount

What You Can Skip:

- Permanent life insurance (unless estate planning needs)

- Accident insurance (if you have adequate disability coverage)

Total Approximate Monthly Investment: $400-900

AGES 40-49: PEAK EARNING AND PROTECTION NEEDS

Your 40s represent peak earning potential and often maximum financial responsibilities. Insurance needs are at their highest.

Essential Coverage:

Auto Insurance:

- Full coverage including comprehensive and collision

- Maintain $2 million+ liability limits

- Consider umbrella policy ($1-2 million additional liability)

- Monthly Cost: $150-400

Home Insurance:

- Ensure replacement cost keeps pace with renovation costs

- Review coverage annually as home value increases

- Maintain adequate liability limits

- Monthly Cost: $120-250

Life Insurance:

- Maintain term life insurance: $500,000-$1,500,000 depending on:

- Remaining mortgage balance

- Children’s education costs

- Income replacement needs

- If you bought term insurance in your 30s, premiums remain locked at lower rates

- If buying new coverage now, expect higher premiums: $80-150/month for $750,000

- Review needs: As debt decreases and kids age, you may need less coverage

Disability Insurance:

- Maximum importance—you’re approaching peak earnings

- Ensure coverage extends to age 65

- Review “own occupation” definition carefully

- Monthly Cost: $150-300 (2-3% of income)

- Don’t reduce coverage: This is not the time to cut corners

Critical Illness Insurance:

- Consider adding if not purchased earlier

- Family history of illness makes this more valuable

- Monthly Cost: $75-200

Long-Term Care Insurance (Consider):

- Premiums are more affordable in your 40s than 50s+

- Consider if you want to age at home vs. facility

- Monthly Cost: $100-250

What You Can Skip:

- Accidental death insurance (redundant if you have life insurance)

- Travel insurance add-ons from credit cards often suffice

Total Approximate Monthly Investment: $600-1,350

AGES 50-59: TRANSITIONING TOWARD RETIREMENT

Your 50s mark the transition toward retirement. Insurance needs begin shifting from income protection to asset preservation and estate planning.

Essential Coverage:

Auto Insurance:

- Continue full coverage

- Maintain high liability limits

- Consider reducing coverage on paid-off older vehicles

- Monthly Cost: $150-400

Home Insurance:

- Critical protection for your largest asset

- Ensure adequate coverage as you approach retirement

- Monthly Cost: $130-300

Life Insurance:

- Assess actual needs: If mortgage is paid off and kids are independent, you may need less

- Term policies purchased in your 30s/40s remain in force at locked-in rates

- Consider 10-15 year term if purchasing new coverage

- New coverage: $150-300/month for $500,000 (significantly higher than younger ages)

- Estate planning: Consider permanent insurance only if you have estate tax concerns or special needs dependents

Disability Insurance:

- Still critical—maintain until retirement

- Most policies end at age 65

- If self-employed, don’t cancel early

- Monthly Cost: $200-400 (premiums increase with age)

Critical Illness Insurance:

- Premium value decreases with age

- Evaluate if existing coverage is sufficient

- Monthly Cost: $150-300

Long-Term Care Insurance:

- Last chance to purchase at reasonable rates

- Premiums skyrocket after age 60

- Monthly Cost: $150-400

What You Can Skip:

- New large life insurance policies (unless specific estate needs)

- Excessive coverage beyond actual needs

Total Approximate Monthly Investment: $700-1,800

AGES 60+: PROTECTING YOUR RETIREMENT

In retirement, your focus shifts from income protection to asset preservation and providing for surviving spouses or dependents.

Essential Coverage:

Auto Insurance:

- Maintain adequate coverage

- Increase liability if your net worth is substantial

- Consider usage-based discounts if you drive less

- Monthly Cost: $150-450 (rates may increase in later years)

Home Insurance:

- Non-negotiable protection for your home

- Ensure adequate replacement cost

- Monthly Cost: $150-350

Life Insurance:

- Assess need carefully: If you don’t have dependents and debts are paid, you may not need coverage

- If needed for surviving spouse, consider:

- Keeping existing term policies if still in force

- Term-to-100 for lifetime coverage at level premiums

- Whole life for estate planning

- New coverage: $200-450/month for $250,000 (very expensive at this age)

- Many retirees: Let term policies expire once kids are independent and assets are sufficient

Disability Insurance:

- Typically ends at age 65

- Not needed once retired

Long-Term Care Insurance:

- If not purchased earlier, likely too expensive now

- Consider self-funding through retirement savings

- Government programs (CPP, OAS) provide minimal support

Critical Illness Insurance:

- Evaluate if premiums justify benefits at advanced age

- May be better to self-insure

What You Can Skip:

- Disability insurance (you’re retired)

- New large life insurance policies unless estate planning needs

- Accident insurance

Total Approximate Monthly Investment: $300-850

GENDER CONSIDERATIONS IN INSURANCE PLANNING

While insurance needs are primarily driven by life stage rather than gender, there are some gender-specific considerations:

Women’s Insurance Considerations:

Life Insurance:

- Women generally pay 5-10% less than men for life insurance due to longer life expectancy

- Stay-at-home mothers should have life insurance covering childcare and household management costs

Disability Insurance:

- Women may pay slightly higher disability premiums due to historically longer claim durations

- Pregnancy and childbirth are typically excluded from disability coverage

- Critical: Women are more likely to experience long-term disabilities

Critical Illness:

- Women should prioritize critical illness coverage given higher breast cancer rates

Men’s Insurance Considerations:

Life Insurance:

- Men pay 5-10% more than women due to shorter life expectancy

- Higher rates for physically demanding occupations (construction, trades)

Disability Insurance:

- Men in high-risk occupations pay significantly higher disability premiums

- Construction workers may pay 2-3x more than office workers

Auto Insurance:

- Young men (under 25) pay significantly higher auto insurance premiums

- Rates equalize with women by age 30

QUICK-WIN STRATEGIES: IMMEDIATE COST REDUCTIONS

Looking for fast savings? Implement these strategies today:

- Call your insurer and ask about available discounts (10 minutes, potential savings: $100-500/year)

- Bundle all policies with one provider (30 minutes, potential savings: $300-800/year)

- Increase deductibles (10 minutes, potential savings: $200-600/year)

- Remove unnecessary coverage (older vehicles, over-insurance) (20 minutes, potential savings: $300-1,000/year)

- Shop competitors for quotes (1-2 hours, potential savings: $500-2,000/year)

Total Potential Annual Savings: $1,400-4,900

COMMON INSURANCE MISTAKES TO AVOID

- Under-insuring to save money: Inadequate liability or life coverage can be catastrophic

- Letting policies automatically renew without shopping: Loyalty doesn’t pay in insurance

- Not reviewing coverage annually: Your needs change; your insurance should too

- Canceling coverage during financial stress: Gaps in coverage can make you uninsurable

- Buying insurance you don’t need: Mortgage life insurance, credit card insurance, extended warranties

- Not disclosing information accurately: Can lead to denied claims

- Filing small claims: Better to pay out-of-pocket for amounts close to your deductible

THE BOTTOM LINE

Insurance is a critical component of financial security, but you don’t need to overpay. By implementing the strategies in this guide, most Canadian families can reduce their total insurance costs by 20-40% while maintaining or even improving their coverage.

Remember:

- Buy life and disability insurance young to lock in low rates

- Bundle policies for automatic discounts

- Shop the market every 1-2 years

- Maintain good credit and driving records

- Invest in risk-reduction (home improvements, anti-theft devices)

- Adjust coverage as life changes (marriage, children, retirement)

Your ideal insurance portfolio will evolve throughout your life. Review your coverage annually, particularly at major life milestones, to ensure you’re adequately protected without overpaying.

Pro Tip: Work with an independent insurance broker who can compare multiple insurers and provide unbiased advice. Their services are typically free (they’re paid by insurers), and they can save you significant time and money.

Insurance shouldn’t break your budget—it should protect it. With these strategies, you can achieve comprehensive protection at a price that fits your financial plan.

⚠️ Disclaimer

The information provided in this article is for informational and entertainment purposes only and should not be considered as financial, legal, or insurance advice. Individual circumstances vary, and readers are strongly encouraged to consult their own licensed financial advisor or insurance agent before making any decisions regarding coverage, investments, or financial planning.

For the full disclaimer and terms of use, please refer to the Detailed Disclaimer Section on captainyourlife.blog.

📖 Further Reading & Trusted Resources

Looking to explore more about insurance costs and savings in Canada?

Here are some credible, up-to-date resources worth checking out:

- 🔹 Insurance Bureau of Canada – Industry Resources & Data

- 🔹 Statistics Canada – Impacts of Rising Auto Insurance Costs (2025)

- 🔹 CLHIA – Canadian Life & Health Insurance Facts (2024 Edition)

- 🔹 Fraser Institute – Comparing Auto Insurance Across Canada

- 🔹 PolicyAdvisor – Disability Insurance Costs & Tips (2025)

- 🔹 Financial Consumer Agency of Canada – Disability Insurance Overview

- 🔹 CAFII – Insurance Among Canadian Homeowners Report

- 🔹 Transport Canada – Motor Vehicle Collision Statistics (2022)

- 🔹 Ratehub.ca – Life Insurance in Canada (2025 Overview)

- 🔹 Canada Drives – Average Car Insurance Costs by Province</li_