Managing your money in today’s unpredictable world is like steering a ship through stormy seas. Without a clear system and regular course corrections, it’s too easy to drift off course—or worse, hit financial shoals. In this article, you’ll discover my Four-Account System and how a weekly financial review keeps me on track, even in choppy economic waters.

From Ocean Navigation to Budget Management

Back in my sailing days, we plotted the vessel’s position using GPS and astronomical sights, then compared that to our dead-reckoning estimate. If we’d drifted, we’d correct our course to avoid danger. In personal finance, rising living costs, job instability, and soaring healthcare or education expenses are the “treacherous waters” of modern life.

As Benjamin Franklin noted: “Beware of little expenses; a small leak will sink a great ship.” This principle underpins my approach.

Why Weekly Financial Reviews Make All the Difference

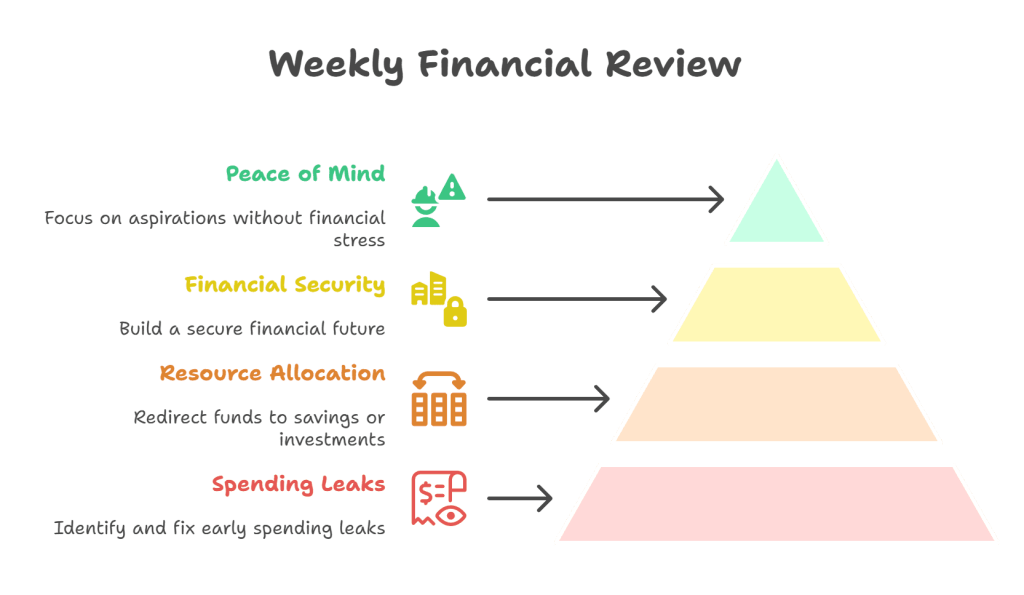

Every single week, I make it a point to slow down and conduct a detailed, structured review of my income, expenses, and investments, comparing them carefully against my monthly financial plan. It’s a disciplined routine—much like a ship’s captain checking the vessel’s exact position and course before navigating into rough weather. By committing to this weekly financial review, you give yourself the ability to:

- Identify and address small spending leaks before they grow into major financial setbacks.

- Proactively redirect extra funds toward your savings targets or long-term investment goals.

- Stay consistently aligned with your overall financial strategy, fostering both long-term stability and peace of mind.

The Four-Account System: A Strong Financial Compass

Here are the four dedicated bank accounts I recommend, each serving a clear purpose:

1. Earnings Account

All income—salary, side gigs, passive earnings—lands here. This is your main hub from which money flows to the other three accounts.

2. Expenses Account

This covers all outgoings: groceries, bills, fuel, repairs, subscriptions. With separated spending, tracking and analyzing is effortless.

3. Investment Account

This is for buying ETFs, stocks, bonds, gold, crypto, and maximizing retirement vehicles like TFSA or RRSP in Canada (or your country’s equivalents). Have a financial advisor help tailor your strategy or dive into research if you’re self-managing.

4. Contingency Fund (High-Interest Savings)

This is your emergency fund—digital life raft. Build 6–8 months of bare-minimum expenses here for stability.

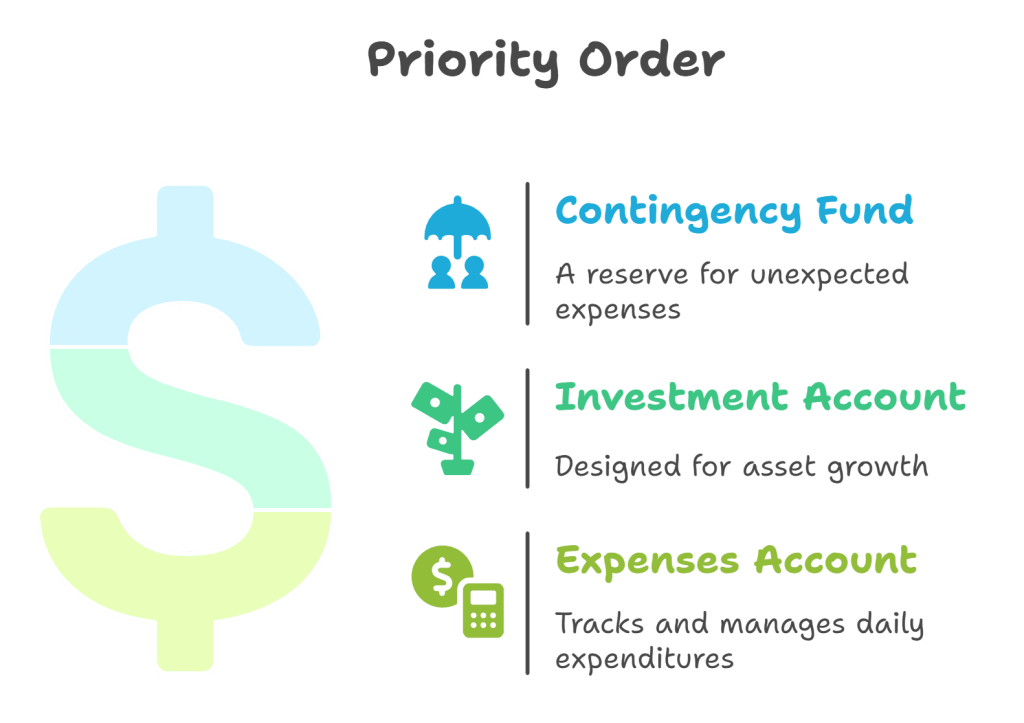

Vital advice from Morgan Housel in The Psychology of Money: “The ability to do what you want, when you want, for as long as you want, has an infinite ROI.”

Warren Buffett advises, “Do not save what is left after spending; spend what is left after saving.” That’s why money flows in this priority order:

- Contingency Fund

- Investment Account

- Expenses Account

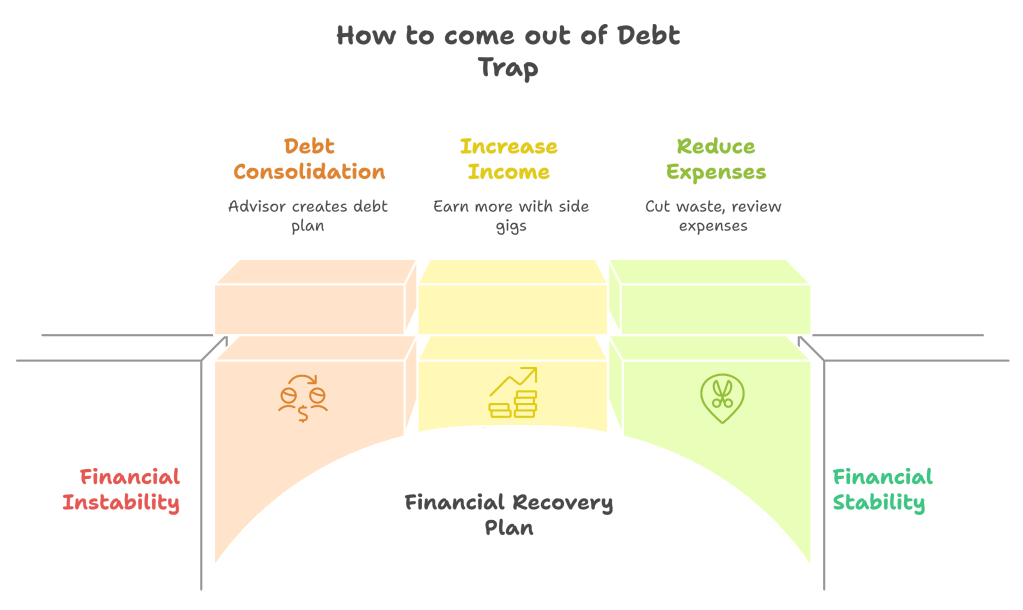

Putting the System to Work, Even Under Pressure

If you’re in debt or tight on cash:

- Consult a certified financial advisor for a debt repayment plan.

- Boost your income—deliver food, drive for rideshare, or freelance.

- Cut waste—track spending in your separate Expenses Account and audit what’s essential vs. avoidable.

Dave Ramsey reminds us: “A budget tells your money where to go instead of wondering where it went.”

Why the Contingency Fund Comes First

Think of this particular account as your financial peace-of-mind standby—a reliable safety net that’s there for you when life throws unexpected challenges your way. While it’s true that investing this money could potentially yield higher returns over time, the primary purpose of this account is to maintain liquidity and provide a secure, easily accessible reserve. This means your funds remain safe, protected from market fluctuations, and available whenever you need them most. Once you’ve fully funded this emergency reserve to cover your essential expenses for several months, you can confidently redirect the money you were setting aside here toward your investment accounts to seek greater growth and long-term wealth accumulation.

Building the Habit: Weekly Review to Financial Confidence

Commit to weekly reviews for the first few months:

- Income tracking: Which gigs give the best time-vs-money returns?

- Expense audit: Can the new iPhone wait if the old one works fine?

- Portfolio update: Stay calm—compounding takes time.

- Emergency fund check: Is it keeping pace with rising costs?

If self-doubt hits, check your contingency balance—it’s your financial safety blanket.

Final Thoughts: Why It Works

The Four-Account System gives you a solid structure to manage your money without feeling like you’re stuck in a rigid box. Think of it like having different jars for different purposes—when you separate your money, prioritize savings, and keep up with regular check-ins, it’s easier to stay on top of things. Imagine it like tending a garden: you water the plants that need it most and pull out the weeds before they take over. Do this consistently, and you won’t just get by—you’ll actually grow your financial health and thrive.

Peter Drucker put it best: “What gets measured gets managed.” With consistent reviews, you can manage your finances with confidence.

Further Reading & Resources

If you’d like to dive deeper into the ideas behind the Four Account System, the following books offer timeless lessons on money and wealth. You can explore more about each title below — and if you wish, purchase them through the affiliate links to support the blog at no extra cost to you:

- Housel, Morgan. The Psychology of Money

- Buffett, Warren. Berkshire Hathaway Annual Letters

- Ramsey, Dave. The Total Money Makeover

- Franklin, Benjamin. Poor Richard’s Almanack