Today, I’m writing about one of the most important report cards we all receive and use — and no, it’s not from school, college, or our workplace. This score quietly updates every month and shapes almost every major financial decision in our lives: our credit score. While it’s tempting to believe that avoiding debt entirely is the safest route, in today’s world, debt is often unavoidable. The truth is, debt is like a double-edged sword — used wisely, it can be a powerful ally in building wealth; mismanaged, it can be financially devastating. The difference comes down to one thing: our relationship with debt and how we choose to manage it.

When I first moved to Canada, I thought I had my finances under control. In India, I’d used credit cards responsibly, paid my bills on time, and even cleared loans ahead of schedule. But upon arrival, I was starting from zero as my Indian credit history meant nothing here. Without a Canadian credit score, I ran into obstacles everywhere: landlords wanted large deposits, credit cards came with high fees and low limits, and car financing wasn’t an option.

I quickly learned that in Canada, credit is king. Whether you’re buying a home, renting an apartment, applying for a mobile plan, or even certain jobs — your credit score plays a critical role. That realization sparked my mission to understand the Canadian credit system, build my score quickly, and maintain it for long-term financial health.

What is a Credit Score?

Think of your credit score as your financial report card.

It’s a three-digit number, usually between 300 and 900, that tells lenders how likely you are to pay back money you borrow.

In Canada, there are two main companies that calculate and issue your credit score:

- Equifax Canada

- TransUnion Canada

How is Your Credit Score Calculated?

Both agencies use similar formulas, but the exact recipe is a bit of a secret. Still, financial experts agree that these are the main factors and their approximate weight:

| Factor | Weight (%) | What It Means |

| Payment History | 35% | Whether you pay your bills on time |

| Credit Utilization | 30% | How much of your available credit you use |

| Credit History Length | 15% | How long you’ve had credit accounts |

| Credit Mix | 10% | Variety of credit types (credit card, loan, mortgage) |

| Recent Inquiries | 10% | How often you apply for new credit |

(Source: Adapted from Equifax Canada consumer education materials)

Example Calculation

Imagine you have:

- A $5,000 limit on your credit card and you use $1,500 → Utilization = 30% (Good)

- You’ve never missed a payment → Payment history = 100% on-time (Excellent)

- Credit account for 2 years → History length is short (Average)

With these numbers, you could expect a credit score around 720-740. If you reduce utilization to 10%, you could push it above 750.

Why Does Your Credit Score Matter?

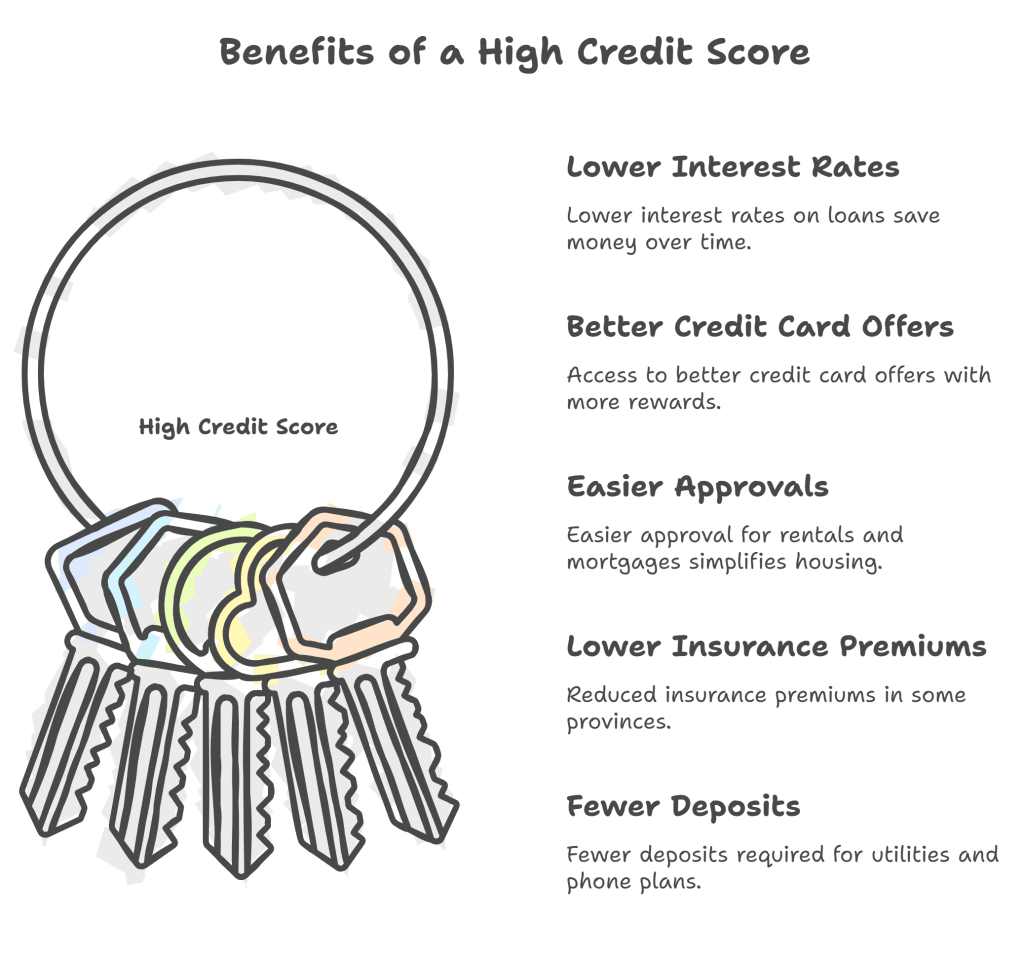

A higher credit score means:

Lower interest rates on loans

Better credit card offers

Easier approval for rentals and mortgages

Lower insurance premiums (in some provinces)

Fewer deposits required for utilities and phone plans

A low score can cost you thousands in extra interest over your lifetime.

How to Check Your Credit Score in Canada

For the full credit report, get it directly from:

- Equifax Canada (free once a year)

- TransUnion Canada (free once a year)

- Your bank’s app (many banks like RBC, BMO, Scotiabank, and CIBC show your score for free)

How Often Should You Check It?

Once a month is fine for most people. Checking your own score is a soft inquiry, which doesn’t hurt your score. Just avoid applying for multiple credit products in a short time, because hard inquiries do lower your score slightly.

Steps to Improve Your Credit Score

- Pay Bills On Time — Every Time

Even one missed payment can drop your score by 100 points. - Keep Credit Utilization Low

Try to use less than 30% of your total limit.

Example: If your limit is $10,000, spend no more than $3,000 before paying it off. - Don’t Close Old Accounts

The longer your history, the better. - Limit Hard Inquiries

Space out applications for loans or credit cards. - Have a Mix of Credit

A credit card + a small personal loan shows you can handle different credit types.

Hacks, Tips & Tricks to Keep Your Score Above 750

- Make Micropayments: Pay off your credit card balance multiple times a month to keep utilization low.

- Increase Your Credit Limit: Call your bank to request a higher limit, but don’t spend more.

- Use a Secured Credit Card: Great for newcomers or rebuilding credit.

- Automate Payments: Set up autopay for at least the minimum amount.

- Become an Authorized User: Get added to a family member’s old, well-managed credit card.

Debt — Friend or Foe?

Debt is like fire.

Managed well, it can keep you warm (help you buy a home, invest in education, build wealth).

Managed poorly, it can burn your house down (cause financial stress, high interest payments, bankruptcy).

Your credit score tells the world whether you’re someone who handles fire with care — or plays with matches.

Recommended Books on Credit & Debt (Available on Amazon.ca)

- Credit Repair Kit for Dummies – Steve Bucci

- The Total Money Makeover – Dave Ramsey

- Your Score: An Insider’s Secrets to Understanding, Controlling, and Protecting Your Credit Score – Anthony Davenport

- The Barefoot Investor – Scott Pape

- Debt-Free Forever – Gail Vaz-Oxlade

Final Word

When I started my journey in Canada, my credit score was nonexistent.

Through careful planning, low utilization, and on-time payments, I crossed my target in less than three years.

If you treat your credit score like a real report card — something you care about improving — you’ll soon see the rewards in lower interest rates, easier approvals, and a lot less stress.

Remember: Debt isn’t bad. Mismanaged debt is.

Learn the rules of the credit game, and you can win it.